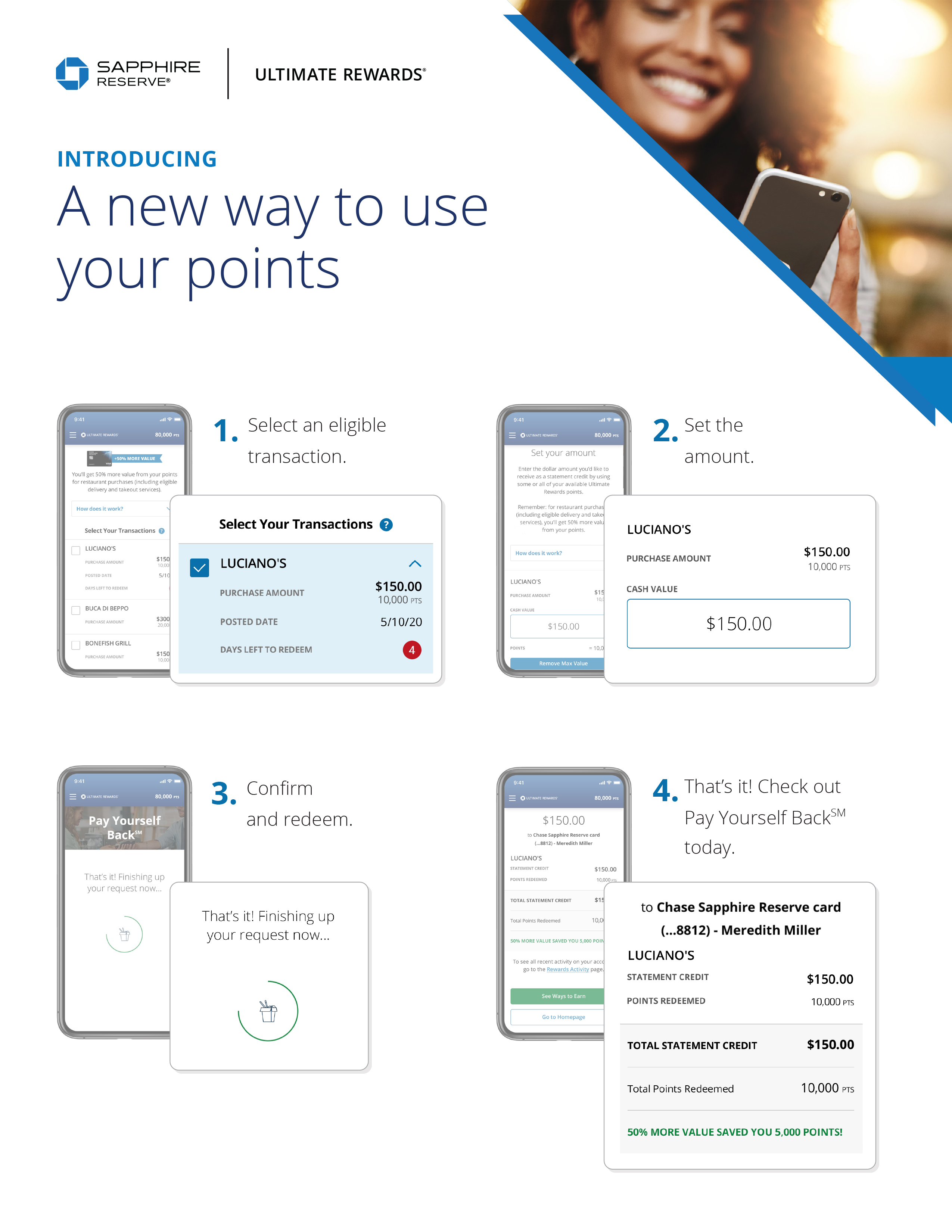

A cash-out refinancing: A cash-aside refinance is a mortgage that replaces your existing mortgage. Out of that new mortgage, you receive a lump-sum single payment, which can be used to build an ADU (or for any other purpose).

If you don’t have far equity in your home, you can still find choices regarding financing your ADU.

Cash: If you don’t have far guarantee but i have savings, having fun with cash is another way to money the building off a keen ADU.

Financial support courtesy good prefab ADU manufacturer: Of a lot providers of prefabricated ADUs provides financing choice that actually work from inside the an identical treatment for conventional home loans.

401k, IRA, or any other later years checking account: Remember, that if you is younger than just 59.5, you’ll likely pay a punishment. Weigh the newest profits on return you could get out of building your ADU, like leasing income and you can enhanced worth of, to decide if this is the right choice to you.

Advantages of choosing a house collateral line of credit getting an ADU

Its safer than simply tapping into advancing years money and maybe against economic charges. Moreover it does not have any to help you protentional filter systems their relationships in the method borrowing off relatives.

For those who have enough collateral accumulated of your home, using you to definitely collateral to invest in their ADU is the greatest alternative as a result of the straight down rates of interest than many other brand of traditional loans

Low interest: A home guarantee line of credit, otherwise HELOC, always has a low interest of about cuatro-7%. This is because its safeguarded by your property, therefore causes it to be a much more reasonable solution than old-fashioned, unsecured loans.

Taxation deductions: Building an enthusiastic ADU can fall under the fresh new Income tax Cuts and you will Operate Operate (TCJA, 2017) criteria which enables one subtract attract paid for the a good HELOC or house guarantee loan. Based on so it income tax law, one taxation paid down for the property guarantee loan or distinctive line of borrowing from the bank regularly “buy, generate, or substantially raise” most of your residence will likely be subtracted out of your taxes (as much as $750,000 within the money getting combined filers, otherwise $325,000 to own solitary filers). Needless to say, you should always get in touch with a taxation professional to ensure so it applies to your specific problem.

Deferred costs to your financing dominant: Having a beneficial HELOC, you first only build repayments to the focus, and just beginning to reduce the principal when you enter into the latest repayment period. It means you could begin assembling your project immediately and you may waiting unless you understand the economic positives (out-of leasing earnings or improved worth of) before you begin and then make huge money.

Detachment and you can payment autonomy: It’s impossible understand how much cash one build opportunity will surely cost. Good HELOC should be of use because you can withdraw financing because the he or she is required and do not have to pay appeal on the more currency that you may possibly not require to own building the ADU. And although you don’t have to build money for the dominant amount into the detachment period, of a cash advance america lot HELOC choices enables you to lower their dominating versus punishment. This provides your better liberty when it comes to building.

Improved borrowing fuel: When comparing to cash-aside refinancing and private fund otherwise structure financing, an excellent HELOC constantly will provide you with entry to increased money in check to build the fresh ADU that suits your circumstances.

Its important to remember, that every financing possibilities include threats. Imagine most of the threats and you will professionals very carefully before deciding how to most readily useful money your ADU. Family security outlines always have upfront closing costs and you can assessment costs which need become considered on your own final decision. It is very important so it will be easy to continue and work out repayments on your primary financial as well because make monthly payments. If you fail to make money towards a HELOC, you run the risk regarding property foreclosure on your domestic.